- 31 MAY 2021

- RESEARCH BULLETIN NO. 84

How has the COVID-19 crisis affected different households’ consumption in the euro area?

The coronavirus (COVID-19) pandemic has generated a complex economic shock that has affected households across the euro area very differently. In studying the impact of this shock on household consumption and the implications for the economic outlook it is critical to understand and factor in these large divergences. In this article, we use rich data from the Consumer Expectations Survey, a new ECB household survey that interviews around 10,000 households across the six largest euro area economies on a monthly basis. We document substantial divergences in pandemic-induced financial concerns of households across population subgroups and countries, with financial concerns being significantly higher for younger, female, and low-income individuals in countries where the first wave of COVID-19 was more severe. Also, we show how these concerns can account to a large extent for the drop in aggregate household spending in 2020. Reflecting this heterogeneity, our results imply that fiscal measures will be most effective in stabilising aggregate consumption and supporting economic recovery if they target the most vulnerable groups with the greatest financial concerns.

Household financial concerns due to COVID-19

According to aggregate data for the euro area, household spending dropped by almost 7% in 2020 compared with 2019. The drop was stronger in France (-8.1%), Spain (-10.9%) and Italy (-8.9%). To understand how consumption adjusted at the household level, in our recent study (Christelis, Georgarakos, Jappelli and Kenny, 2020) we exploit household-specific information on how severe the financial consequences of the COVID-19 pandemic are perceived to be. One would expect pandemic-induced financial concerns to negatively associate with consumption for several reasons. First, financial concerns depend on current income, access to liquidity and accumulated wealth, with less wealthy households being less equipped to buffer the adverse consequences of the COVID-19 outbreak. Second, financial concerns are associated with lower income expectations (e.g. due to the lockdown measures), depending on the occupation, sector of activity and remote working capability of household members. Third, financial concerns could reflect an increase in uncertainty about the future, because some households fear a higher probability of becoming unemployed, or because there is uncertainty about the duration of the crisis and the economic consequences of further COVID-19 waves. Financial concerns could also reflect other household-specific factors ranging from, for example, household size to concerns about future increases in the tax burden.

A growing number of studies investigate the consumption effect of the pandemic in the United States and in Europe, relying mostly on administrative data.[2] They typically identify the effect on consumption using area-level measures of the COVID-19 impact (e.g. deaths per region). Notably, they do not rely on a household-specific measure of exposure to the COVID-19 shock that can capture the highly heterogeneous nature of the pandemic’s effect across different households.

We use rich panel data from the Consumer Expectations Survey (CES), a new ECB survey that was launched as a pilot in January 2020. Since April 2020 the survey has been running at its target sample size, interviewing around 10,000 households across the six largest euro area economies (Germany, France, Italy, Spain, the Netherlands and Belgium) on a monthly basis.[3] The panel dimension of the CES data means that respondents are surveyed repeatedly, which is particularly important as it ensures that the dynamic response of the same households can be studied over time. The survey is representative of the underlying populations and collects via the internet high-frequency and fully harmonised information on households’ demographics, income and consumption and on how households perceive the economic consequences of the pandemic. For many variables we are able to exploit the panel nature of the survey from April to October 2020.

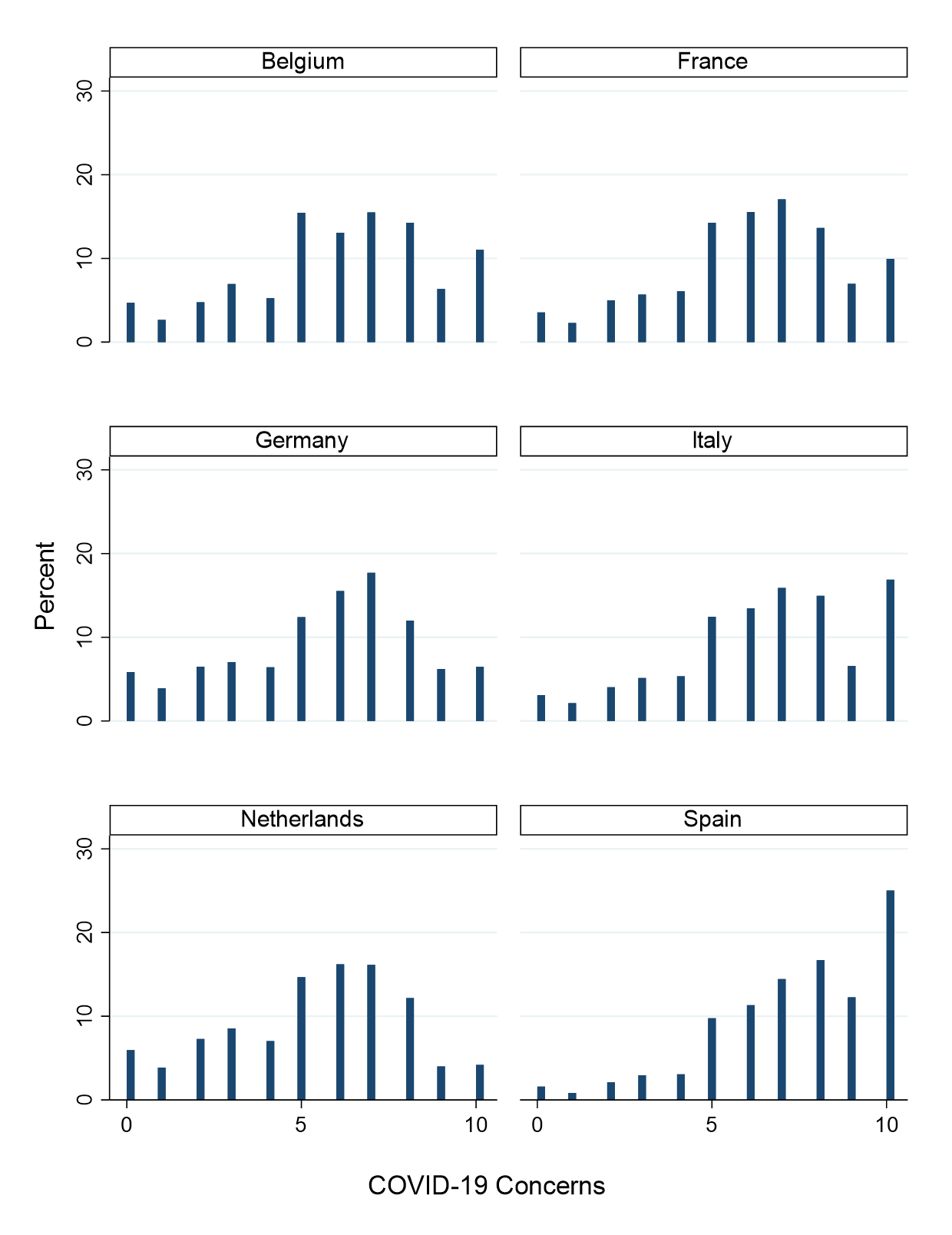

Figure 1

How concerned households are about their financial situation owing to COVID-19

Consumer Expectations Survey data April – October 2020

(y-axis: share of households in percent, x-axis: level of concern with range 0 (“not at all concerned”) to 10 (“extremely concerned”)

Note: The figure shows the fraction of responses per level of COVID-19 financial concern and by country. Data are drawn from the April, July and October waves of the CES.

The survey asks respondents the following question on the economic impact of the pandemic: How concerned are you about the impact of the coronavirus (COVID-19) on the financial situation of your household? (coded from 0, “not concerned”, to 10, “extremely concerned”). Figure 1 plots the distribution of household financial concerns due to COVID-19 within the six countries included in our study in the form of a histogram. The share of respondents concerned about their financial situation is higher in those countries that during the first wave of the pandemic experienced the highest number of COVID-19 cases and deaths, and stricter lockdown policies limiting citizens’ mobility and engagement in economic activity. In Italy and Spain 36% and 52% of respondents, respectively, express high concerns (7 or above) about the financial consequences of COVID-19. Indeed, these two countries stand out with a significant fraction of households reporting the highest possible level of concern (10). On the other hand, in Germany and the Netherlands the fractions expressing relatively high concerns (above 7) are 25% and 20%, respectively.

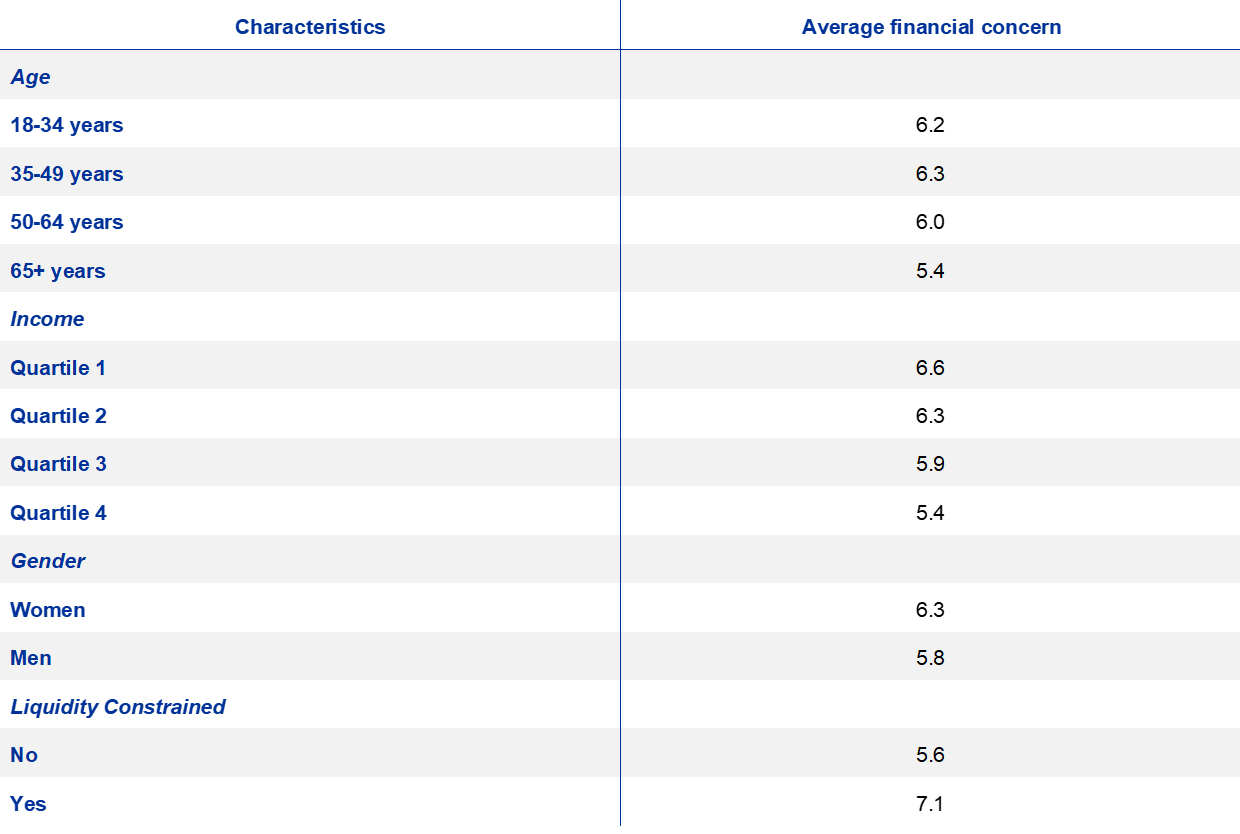

Further analysis shows that such financial concerns are not distributed evenly across the population. As shown in Table 1, the pandemic has induced higher financial concerns in younger age groups compared with those older than 65 years, many of whom have retired and are thus more likely to be more insulated from income shocks arising from the crisis. In addition, financial concerns due to COVID-19 are higher among lower income households and households that are liquidity-constrained (i.e. report that they are not able to meet an unexpected payment equal to one month of their household income). Furthermore, female respondents generally report higher overall financial concerns. The survey also includes separate questions on the health consequences of COVID-19 for the respondent and his or her household. Unlike financial concerns, health-related concerns are considerably higher among the older (65+) and the middle-aged (36-64) households compared with the young. However, formal econometric analysis shows that the effects of the COVID-19 outbreak on consumption mainly operate through households’ perceptions about the financial repercussions of the shock and not via their concerns about the effects of the pandemic on their own health.

Table 1

Differences in financial concerns due to COVID-19 across demographic groups

Consumer Expectations Survey data April – October 2020

(average based on a scale of 0 (“not at all concerned”) to 10 (“extremely concerned”))

Source: ECB Consumer Expectations Survey. Using weighted data. Individual-level concerns about the household’s financial situation have been elicited on a monthly basis since April by asking: “How concerned are you about the impact of coronavirus (COVID-19) with respect to the financial situation of your household?”, with an 11-step response scale ranging from 0 (not at all concerned) to 10 (extremely concerned). Liquidity constraints are inferred from the ability of a household to meet an unexpected payment equal to one month of household income.

How households adjusted their consumption in response to the COVID-19 shock

In Figure 2 we plot binned values of the (logarithm of) monthly non-durable consumption against the values of the measure of COVID-19 financial concerns (0-10) discussed above. Comparing those who are least concerned about the financial consequences of COVID-19 (values of 2 and below) with those that are very concerned (9 or 10) implies a reduction in consumption of about 25%. Of course, this relation does not consider other variables that affect consumption. Econometric estimates, controlling for other variables, indicate that raising concern from 0 (the least concern) to 6 (the median concern) reduces consumption by 8.2%. On the other hand, concern about COVID-19’s impact on one’s own health as well as the health of other household members has no statistically significant impact on consumption. The results suggest that financial concerns are a much stronger independent driver of spending behaviour than health-related concerns whose effects may instead be transmitted via the impact on the household’s expected financial conditions (e.g. if a job loss were to arise as a result of health problems). Moreover, as our estimation controls for current income, socio-economic variables, unobserved household traits (e.g. risk attitudes) and aggregate effects (e.g. country macroeconomic conditions), precautionary saving is a likely explanation for the negative association between COVID-19 financial concerns and consumption.

Figure 2

Households’ concern about their financial situation due to COVID-19 and the effect of this concern on consumption

Consumer Expectations Survey data April – October 2020

(y-axis: Log consumption, x-axis: level of concern with range 0 (“not at all concerned”) to 10 (“extremely concerned”)

Note. The figure shows a scatterplot and a fitted line of the natural logarithm of monthly non-durable consumption against the COVID-19 financial concern. Data are binned. Data are drawn from the April, July and October waves of the CES.

Conclusions

The study suggests that easing pandemic-related financial concerns can counter the observed drop in spending and can reduce the extent to which households adjust their consumption in response to negative income shocks. In particular, the large divergences in financial concerns across households suggest that highly targeted government interventions that aim to lessen the financial concerns of younger households, lower income households and households with less stable employment conditions will support consumption of these groups and contribute to economic recovery.

References

Andersen, A., Hansen, E.T., Johannesen, N. and Sheridan, A. (2020), “Consumer Responses to the COVID-19 Crisis: Evidence from Bank Account Transaction Data”, Covid Economics, No 7, pp. 88-114.

Baker, R.S., Farrokhnia, R.A., Meyer, S., Pagel, M. and Constantine, Y. (2020), “How Does Household Spending Respond to an Epidemic? Consumption During the 2020 COVID-19 Pandemic”, Covid Economics, No 18, pp. 73-108.

Bounie, D., Camara, Y. and Galbraith, J. W. (2020), “Consumers’ Mobility, Expenditure and Online-Offline Substitution Response to COVID-19: Evidence from French Transaction Data”, CIRANO Working Papers, No 28.

Carvalho, P. B., Peralta, S. and Pereira, J. (2020a), “What and How did People Buy during the Great Lockdown? Evidence from Electronic Payments”, Covid Economics, No 28, pp. 119-158.

Carvalho, M.V., Hansen, S., Ortiz, Á., García, R.J., Rodrigo, T., Mora, R. S. and Ruiz, J. (2020b), “Tracking the COVID-19 Crisis with High Resolution Transaction Data”, CEPR Discussion Paper, No 14642.

Chetty, R., Friedman, N. J., Hendren, N., Stepner, M. and the Opportunity Insights Team (2020), “The Economic Impacts of COVID-19: Evidence from a New Public Database Built Using Private Sector Data”, NBER Working Paper, No 27431, November.

Christelis, D., Georgarakos, D., Jappelli, T. and Kenny, G. (2020), “The COVID-19 Crisis and Consumption: Survey Evidence from Six EU Countries”, ECB Working Paper, No 2507, December.

Chronopoulos, D., Lukas, M. and Wilson, J.O.S. (2020), “Consumer spending responses to the Covid-19 pandemic: An assessment of Great Britain”, Covid Economics, No 34, 145-186.

Cox, N., Ganong, P., Noel, P., Vavra, J., Wong, A., Farrell, D. and Greig, F. (2020), “Initial Impacts of the Pandemic on Consumer Behavior: Evidence from Linked Income, Spending, and Savings Data”, NBER Working Paper, No 27617, July.

Dunn, A., Hood, K. and Driessen, A. (2020), “Measuring the Effects of the COVID-19 Pandemic on Consumer Spending using Card Transaction Data”, BEA Working Paper, No WP2020-5, US Bureau of Economic Analysis.

Hacioglu, S., Känzig, D. and Surico, P. (2020), “Consumption in the Time of Covid-19: Evidence from UK Transaction Data”, CEPR Discussion Paper, No 14733.

- This article was written by Dimitris Georgarakos and Geoff Kenny (both Directorate General Research, European Central Bank) as well as Dimitris Christelis (University of Glasgow) and Tullio Jappelli (University of Naples Federico II). The authors thank Michael Ehrmann, Alex Popov and Louise Sagar for useful comments. The views expressed here are those of the authors and do not necessarily represent the views of the European Central Bank and the Eurosystem.

- Baker et al. (2020), Cox et al. (2020), and Chetty et al. (2020) for the United States, Chronopoulos et al. (2020), Hacioglu et al. (2020) and Dunn et al. (2020) for the United Kingdom, Andersen et al. (2020) for Denmark, Bounie et al. (2020) for France, Carvalho et al. (2020a, 2020b) for Portugal and Spain.

- See further background on the survey.