Towards a macroprudential stress test and growth-at-risk perspective for climate-related risk

This publication proposes a macroprudential stress test approach to recognise the systemic nature of climate risks. The approach recognises that climate-related risks ingrained in long-term climate-related scenarios, such as those released by the Network for Greening the Financial System (NGFS)[1], add to other deep-seated cyclical and structural risks in economic systems. These risks can accumulate in certain periods and amplify each other, leading to far more negative outcomes than if each of these risk sources existed in isolation. Additionally, the approach introduces the concept of dynamic balance sheets that allow banks to adjust to scenario adversity, while noting that some of these reactions can amplify the initial source of stress. By comprehensively quantifying the impact of climate-oriented scenarios on the banking system and an economy, such stress test can inform a timely and well-founded policy response.

Recent years have witnessed growing use of forward-looking analysis of banking sector vulnerability to climate-related risks. De Nederlandsche Bank released its transition risks-focused stress test in 2018.[2] The Europe-wide initiatives in 2020[3] and 2021[4], the Banque de France exercise[5], and the most recent economy-wide European Central Bank (ECB) stress test[6] take a step towards combining transition and physical risks. Findings so far point towards the concentration of future transition risks in certain economic sectors and exposures (see, for example, de Guindos, 2021). The fact that climate related risks affect sectors differently, and that they can take decades to fully materialise, can result in a falsely reassuring assessment of financial system resilience (ECB/ESRB Project Team, 2021[7]). The long-term nature of climate-related scenarios can also challenge common stress testing assumptions, including the constant balance sheet assumption, where banks or firms keep their balance sheet size and structure constant over time, and the lack of the feedback from banks’ reactions impacting the real economy.

The first building block of the macroprudential approach is a semi-structural model with individual banks and amplification mechanisms. The macro-micro model features a macroeconomic block for the 19 euro area economies and a representation of 89 significant banks, covering approximately 70% of the euro area banking system, with their individual balance sheets and profit and loss accounts (Budnik et al., 2020).[8] The model is a well-defined stress testing framework incorporating the pass-through of macro-financial scenarios into credit and interest rate risks, and accounting for market and operational risks. Additionally, banks adjust their lending volumes and prices, liability structure and dividend pay-outs according to economic conditions and their own situation, with the lending decisions feeding back to the real economy (see Figure A).

Figure A

Schematic illustration of the macro-micro model

Banks’ reactions to scenario adversity feed back to the real economy

Source: ECB.

The macro-micro model encapsulates a rich set of macro-financial and idiosyncratic bank-level shocks. The macro-financial shocks, such as to aggregate demand or house prices, and bank-level shocks, e.g. to asset quality, operational risk or lending decisions, are all characterised by their historical distributions. Repetitive stochastic draws from the joint distribution of multiple model shocks generate numerous plausible macro-financial scenarios, spanning from very good economic boost episodes, to deep and lasting recessions.[9] The lower tails of generated distributions of macroeconomic or banking sector variables link to the growth-at-risk (GaR) concept.

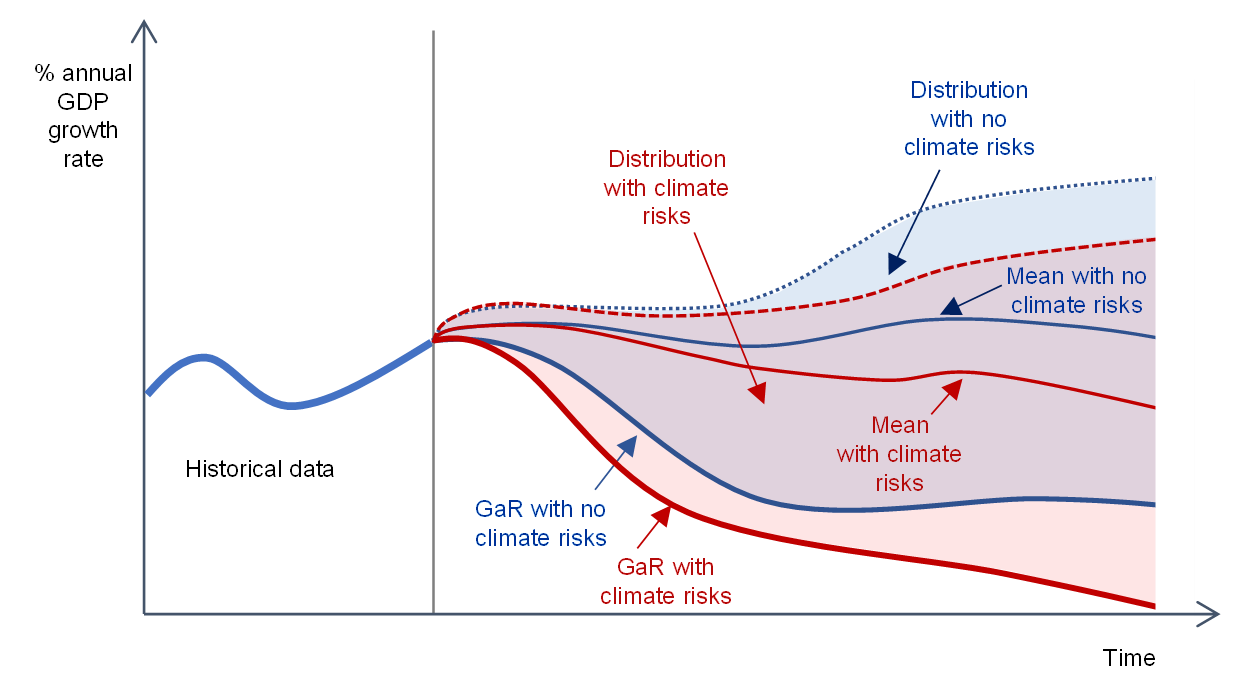

The second building block is the stochastic interpretation of long-run NGFS scenarios. Climate risks shift the long-run trajectory of economic growth. The NGFS scenarios, such as the disorderly transition or “hot house” world, focus on measuring this shift. Figure B illustrates the concept, in a stylised fashion, as the mean shift from the trajectory naively extrapolated from the past data (“mean with no climate risk”) to a growth path that accounts for the realisation of transition and physical risks (“mean with climate risk”). Even in the absence of significant interactions between climate and other macro-financial risks, climate-relevant scenarios will shift the full distribution of economic growth. This also translates into the aggravation of economic recessions, marked by the shift in the GaR, i.e. the lower percentile of the growth distribution.

Figure B

Climate-relevant scenarios and growth distribution

Climate risks add to other sources of macro-financial risks

Source: ECB.

Notes: The blue solid line represents the mean prediction of economic growth with no climate risk. The blue fan spanned between the blue thick line marking a lower percentile and a thin blue line marking an upper percentile represents the distribution of economic growth in the absence of climate risks. The red solid line, and the red fan, represent the mean and the distribution of economic growth in the presence of climate risks.

The banking sector will act as one of the channels through which climate and other macro-financial shocks amplify each other. The cumulation of risks in lower tails of growth distribution will most likely trigger non-linearities in firms’, and later banks’, asset quality, as well as in banks’ decisions. Taking into account the feedback loops between banks’ lending decisions and economic growth, the gap between the GaR and the mean for scenarios emphasising climate risks is likely to be larger than the corresponding gap for scenarios not accounting for climate risks.

The last building block of the approach is the recognition of asymmetric pass-through of climate-related risks onto individual banks’ balance sheets. The vulnerability of individual banks to climate risks depends on the dynamic structure of their exposures to different sectors and geographies. The evolution of climate risks in different sectors and locations should be linked to relevant NGFS scenarios, and in many instances can be described by their full distributions.[10] The stochastic approach can explore these full distributions – e.g. realisations of extreme weather events in any location, rather than using only a fixed-point probability of an extreme weather event – and map them into idiosyncratic bank-level shocks.

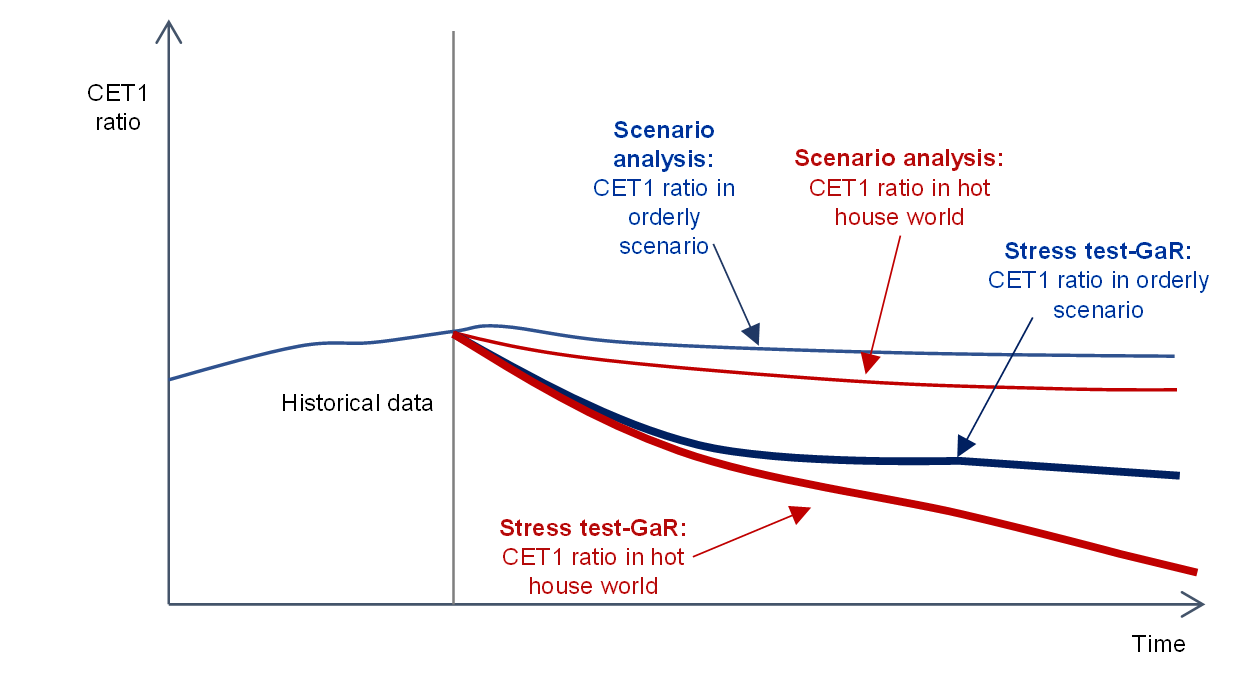

The stylised results of the macroprudential stress test with climate risks are presented in Figure C. The macroprudential stress test will deliver two types of paths for banks’ variables: one set which corresponds with the paths of the original NGFS scenarios analysis (marked by thin lines in Figure C) and another set which corresponds with the concentration of climate and non-climate risks and their amplification in the tails of the distribution (thick lines in Figure C). The former set of outcomes reflects the NGFS scenario analysis, while the latter the related stress test, namely the evolution of the banking system under plausible but sufficiently adverse assumptions.

Figure C

Climate-relevant scenarios and growth distribution

Encapsulating a climate risk scenario analysis and stress test in one framework

Source: ECB.

Notes: The blue thin line represents the stylised conditional forecast of system-level CET1 ratio consistent with the path of the orderly NGFS scenario, while the red thin line represents the system-wide CET1 ratio consistent with the hot house world NGFS scenario. The thick blue and red lines represent the GaR (lower percentiles) of conditional forecasts in both NGFS scenarios.

The climate-focused macroprudential stress test can help to overcome the short-sightedness of management and policy decisions by quantifying their future consequences. Climate change and pertinent economic processes will affect the future of the banking system, even if the magnitude of this impact is highly uncertain. Using the estimates for different scenarios and including these in the GaR method, where risks amass and amplify, can help banks and policymakers prepare for or even influence future outcomes.

References

ACPR (2021), “The main results of the 2020 climate pilot exercise”, Analysis and synthesis, No 122, April.

Budnik, K., Balatti, M., Dimitrov, I., Groß, J., Kleemann, M., Reichenbachas, T., Sanna, F., Sarychev, A., Siņenko, N. and Volk, M. (2020), “Banking euro area stress test model”, Working Paper Series, No 2469, ECB, September.

Budnik, K., Dimitrov, I., Giglio, C., Groß, J., Lampe, M., Sarychev, A., Tarbé, M. and Volk, M. (2021), “The growth-at-risk perspective on the system-wide impact of Basel III finalisation in the euro area”, Occasional Paper Series, No 258, ECB, July.

Budnik, K., Dimitrov, I. and Groß, J. (2020), “Selecting adverse economic scenarios for the quantitative assessment of euro area banking system resilience”, Financial Stability Review, ECB, November.

de Guindos, L. (2021), Shining a light on climate risks: the ECB’s economy-wide climate stress test, ECB, March.

ECB/ESRB Project Team on climate risk monitoring (2020), “Positively green: measuring climate change risks to financial stability”, ECB/European Systemic Risk Board, June.

ECB/ESRB Project Team on climate risk monitoring (2021), Climate-related risk and financial stability, ECB/European Systemic Risk Board, July.

Vermeulen, R., Schets, E., Lohuis, M., Kölbl, B., Jansen, D.-J. and Heeringa, W. (2018), “An energy transition risk stress test for the financial system of the Netherlands”, Occasional Studies, Vol. 16, No 7, De Nederlandsche Bank.

- See the NGFS Scenarios Portal.

- Vermeulen, R., Schets, E., Lohuis, M., Kölbl, B., Jansen, D.-J. and Heeringa, W. (2018), “An energy transition risk stress test for the financial system of the Netherlands”, Occasional Studies, Vol. 16, No 7, De Nederlandsche Bank.

- ECB/ESRB Project Team on climate risk monitoring (2020), “Positively green: measuring climate change risks to financial stability”, ECB/European Systemic Risk Board, June.

- ECB/ESRB Project Team on climate risk monitoring (2021), “Climate-related risk and financial stability”, ECB/European Systemic Risk Board, July.

- ACPR (2021), “The main results of the 2020 climate pilot exercise”, Analysis and synthesis, No 122, April.

- The preview of the stress test results can be found in de Guindos, L. (2021), “Shining the light on climate risks: the ECB’s economy-wide climate stress test”, ECB, 18 March.

- See Chapter 8 and Box 7.

- Budnik, K., Balatti, M., Dimitrov, I., Groß, J., Kleemann, M., Reichenbachas, T., Sanna, F., Sarychev, A., Siņenko, N. and Volk, M. (2020), “Banking euro area stress test model”, Working Paper Series, No 2469, ECB, September.

- The semi-structural approach to the growth-at-risk perspective has been applied to the assessment of financial regulation in Budnik, K., Dimitrov, I., Giglio, C., Groß, J., Lampe, M., Sarychev, A., Tarbé, M. and Volk, M. (2021), “The growth-at-risk perspective on the system-wide impact of Basel III finalisation in the euro area”, Occasional Paper Series, No 258, ECB, July, and to stress testing in Budnik, K., Dimitrov, I. and Groß, J. (2020), “Selecting adverse economic scenarios for the quantitative assessment of euro area banking system resilience”, Financial Stability Review, ECB, November.

- For example, the Four Twenty Seven dataset already used in the ECB economy-wide stress test includes distributions of various extreme weather events by location.